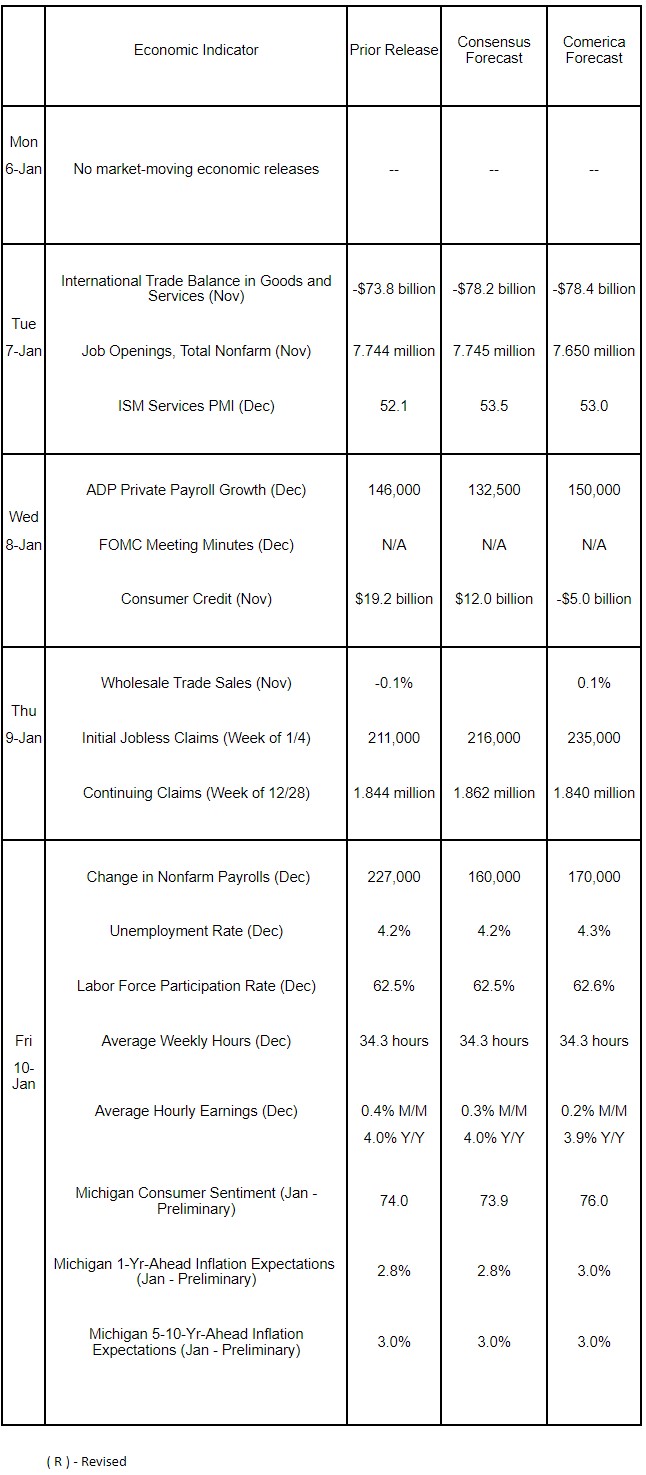

Preview of the Week Ahead

Markets face a busy week of important economic data releases, led by the monthly jobs report. Employers likely added jobs at a slower pace in December after increasing headcount solidly in the prior month. The unemployment rate and the labor force participation rate both likely edged higher, while wage inflation is likely to have eased after hot readings in the prior two months. Released at a lag to the jobs report, vacancies probably fell in November after rising sharply in October.

Markets will intensely scrutinize the minutes of the Federal Open Market Committee’s (FOMC) December meeting after the Committee’s unexpectedly hawkish cut last month. Members’ justifications for raising their inflation projections will be in particular focus, as will their deliberations about the economic impact of the incoming administration’s policies.

The positive spillovers from the election are probably continuing to drive consumer sentiment, with the University of Michigan’s Survey of Consumers likely to have risen to a multi-month high in January. Influenced by short-term energy price increases, households’ year-ahead inflation expectations probably rose, while longer-term inflation perceptions likely remained well-anchored. Sharp increases in gasoline and natural gas prices in the past several days are also putting upward pressure on interest rates, with yields on the benchmark 10-Year Treasury note up half a percentage point since early December. Consumer credit outstanding probably pulled back in November after rising sharply in October.

The trade deficit, which includes cross-border trade in both goods and services, likely widened in November, echoing the advance report on international trade in goods which showed a sharp deterioration.

The Week in Review

The economic calendar was light last week. The manufacturing sector contracted at a slower pace in December than November, according to the ISM Manufacturing PMI, which rose to 49.3% from 48.4% in November. The report’s underlying details were mixed: To the upside, production expanded for the first time since mid-2024, while new orders rose for the second consecutive month. At the same time, manufacturers reduced employment for the seventh consecutive month, and reported paying higher prices for inputs for the third month running.

The S&P CoreLogic Case-Shiller 20-City Home Price Index rose by 0.3% in October. Continuing the disinflationary trend which began early last year, annual home prices rose 4.2% in October, down from 4.6% in the prior month and from 7.5% recorded last March. The FHFA House Price Index rose by 0.4% in October after an unrevised 0.7% increase in September and was up 4.5% on an annual basis for the second consecutive month. Annual house price inflation, as measured by the FHFA index, is also down markedly from its recent high of 7.1% recorded in February 2024.

For a PDF version of this publication, click here: Comerica Economic Weekly, January 6, 2025

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.