Preview of the Week Ahead

President Trump on March 26 signed an executive order raising tariffs on imported cars and light trucks by 25 percent, which he said would become effective on April 3. Financial markets will be on edge as they wait to see if this latest tariff threat is another negotiating tactic or an actual hike. If enacted as pledged, the tariffs would contribute to the faster inflation foreseen by last week’s consumer surveys.

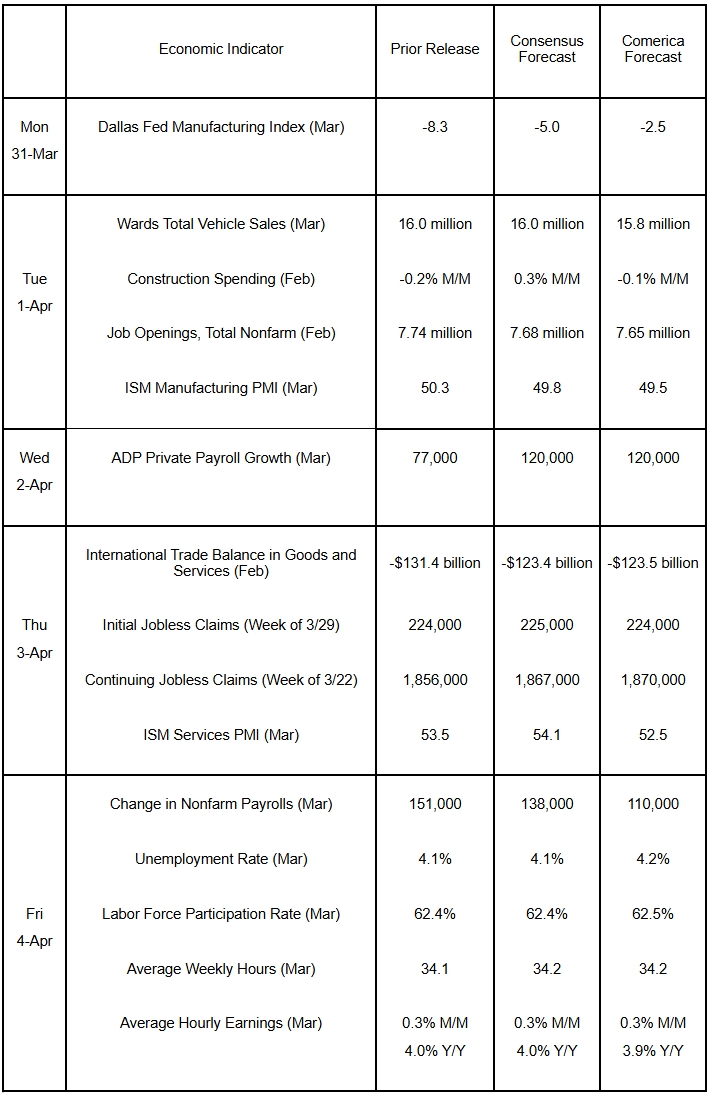

The March jobs report will probably show a modest increase in employment and a small uptick in the unemployment rate. The average workweek is expected to have edged higher, while wages likely rose moderately. Job openings likely eased in February. The ISM Manufacturing PMI will probably report the manufacturing sector slipped back into contraction last month. The ISM Services PMI, on the other hand, is expected to show continued expansion of the services sector, though at a slower pace. Construction spending likely eased in February. The trade deficit in goods and services probably narrowed in February on the back of a lower goods trade shortfall.

The Week in Review

Economic growth in the fourth quarter of 2024 was revised up a hair to 2.4% annualized in the third estimate of real GDP from 2.3% in the second estimate. Real final sales to private domestic purchasers—spending by American households and businesses—rose a solid 2.9% annualized, indicating domestic demand was stronger than the headline figure. For all of 2024, the economy grew a healthy 2.8%, close to 2023’s 2.9% increase.

However, real GDP is likely weakening in the first quarter. The goods trade deficit narrowed to $148 billion in February from a record $156 billion in January, but was still a staggering 60% higher than February 2024. The surge in the trade deficit is mostly due to importers frontrunning higher tariffs. January and February’s large trade deficits will be a big drag on first quarter GDP growth.

Personal income jumped by 0.8% in February, led by sharp increases in government transfers and solid growth of compensation of employees. Personal consumption expenditures rose 0.4%, but were up just 0.1% after adjusting for inflation, following a downwardly-revised 0.6% contraction in January. The first quarter’s weak consumer spending will, like the trade deficit, contribute to an ugly GDP report for the quarter. The PCE Price Index rose 0.3% in February for the third consecutive month, holding annual inflation steady at 2.5%. The core PCE Price Index was a tad hotter than the consensus and rose 0.4% on the month and 2.8% on the year.

Consumer confidence retreated for the fourth consecutive month in March according to The Conference Board’s survey, with the expectations component tumbling to a 12-year low. Year-ahead inflation expectations rose to the highest since April 2023. Consumer sentiment also fell in the final release of the University of Michigan’s consumer survey, with forward-looking expectations the worst since July 2022. In the Michigan survey, year-ahead inflation expectations were the highest since November 2022 and 5-to-10-year inflation expectations the highest since 1993.

For a PDF version of this publication, click here: Comerica Economic Weekly, March 31, 2025

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.