Economy Hit an Air Pocket in January, Lowering 2025’s Growth Prospects;

Tariffs Are Likely to Keep Inflation Above Fed’s Target This Year

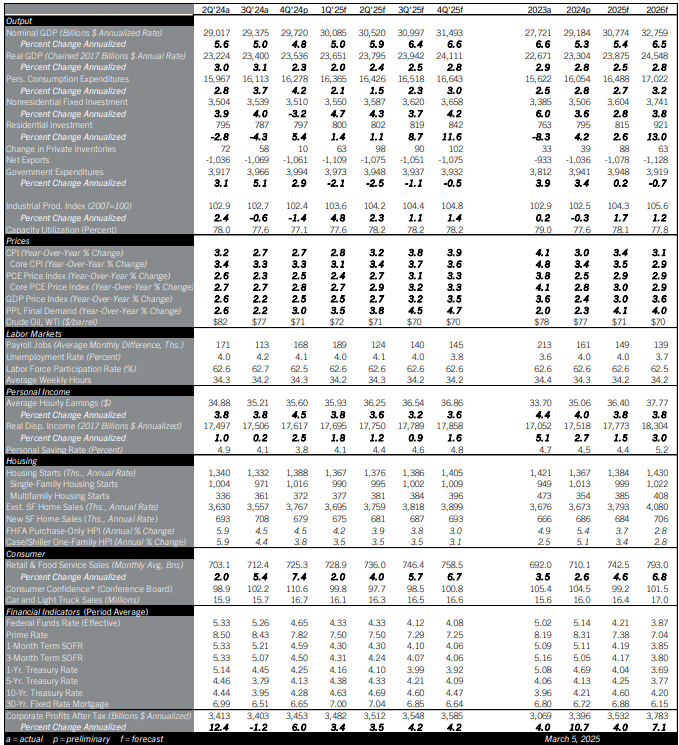

Monthly economic data disappointed in January, with declines in retail sales, auto sales, housing sales, and manufacturing production. A number of one-off drags weighed on the month: The LA wildfires, a bad flu season, and (likely having the largest impact) severe winter weather across much of the continental United States. Even as these headwinds faded in February, new drags appeared. The DOGE cuts to federal headcount and suspended payments for federal programs pushed up jobless claims, and will likely translate to a 250,000 to 500,000 cumulative drag on payroll growth in the next six months. Consumer sentiment jumped after the election, but reversed and weakened in January and February. The University of Michigan’s consumer survey (Which breaks out sentiment by political affiliation) shows the drop is concentrated among Democrat-leaning consumers, who are the most downbeat since 2008. Republican-leaning sentiment is considerably better. But even surveys whose respondents lean right show growing concern about economic uncertainty, in particular related to higher tariffs. The tariff increases proposed in February and March would be equivalent to a tax increase of between 0.5% and 1.0% of U.S. GDP, equivalent to about half of U.S. corporate tax receipts—in other words, a substantial hike. Whether they end up at those levels, higher, or lower, tariff hikes promise to raise prices in 2025 and 2026.

Inflation entered 2025 trending in the right direction. The core PCE index excluding food and energy slowed in January to the smallest year-over-year increase since March 2021. However, the Fed’s focus has shifted from the rear-looking data flow to the forward-looking outlook as tariffs raise goods prices, and as more aggressive immigration enforcement reduces the number of immigrants entering the job market. The Fed also is watching upside pressures on inflation from egg and meat prices as the avian flu sweeps agricultural flocks, and from higher gasoline, diesel, and natural gas prices in January and February. These shocks in combination seem set to keep inflation above the Fed’s two percent target in 2025.

The Fed held rates steady at their January decision and signaled they are in ‘no hurry’ to make further interest rate cuts near-term. Since their decision, financial markets have become unsettled by the January macro slowdown, DOGE, and tariff noise, and have started to price in the possibility of the Fed pivoting to substantial rate cuts by the end of 2025. However, Comerica continues to forecast for the Fed to cut the federal funds target by only a quarter of a percent by year-end, since inflation will remain a source of frustration for them. In addition, Washington will likely start discussions soon on plans to repurpose DOGE’s spending cuts and tax revenues from tariffs to pay for tax cuts in 2026, which the Fed would see as a reason to look past a near-term slowdown. Separately, the Fed is forecast to end the run-off of their balance sheet (a.k.a. “Quantitative Tightening” or QT) in July.

For a PDF version of this publication, click here: March 2025 U.S. Economic Outlook

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.